Did President Trump just call for federal regulation of the health insurance industry?

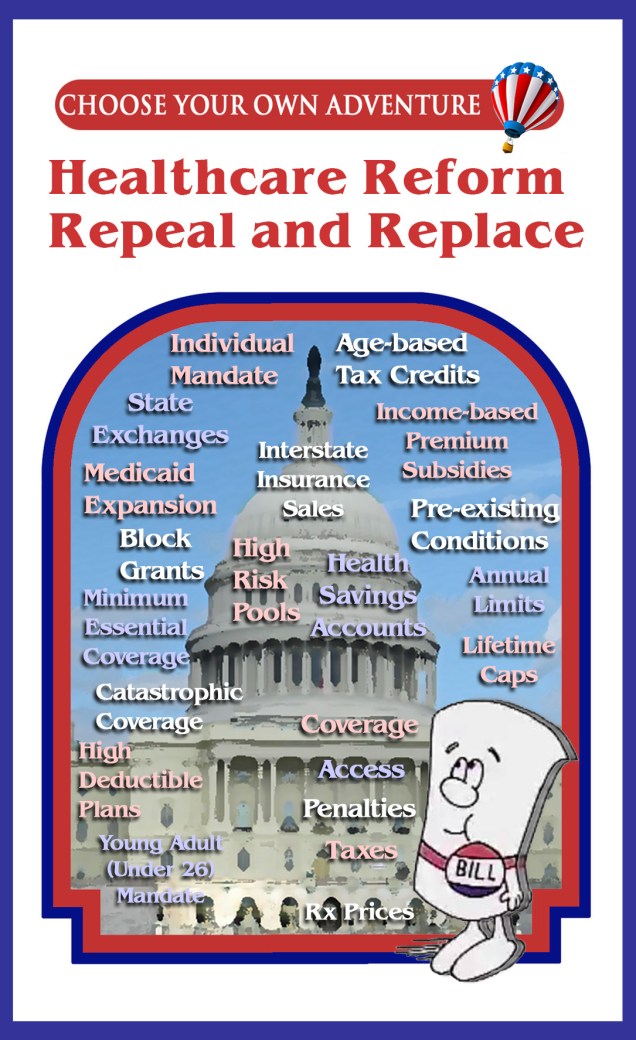

In his first address to Congress, President Trump enumerated his healthcare reform priorities. These include protecting coverage for those with pre-existing conditions, tax credits, health savings accounts, giving states more flexibility on Medicaid, and bringing down prescription drug prices. Then he said this:

…the time has come to give Americans the freedom to purchase health insurance across state lines…

This last line is the one we should remember. Allowing insurers to sell across state lines will require uniform regulations and will inevitably move us toward a system of federal health insurance regulation. Whether he intended it or not, Trump just succeeded in undermining the state regulation of insurance.

Interstate insurance sales have long been a component of Republican healthcare legislation and part of an ongoing debate about state vs. federal insurance regulation.

The Empowering Patients First Act (H.R. 3400) first introduced in 2009 and sponsored by then Rep. Tom Price (now Secretary of Health and Human Services) contains the following:

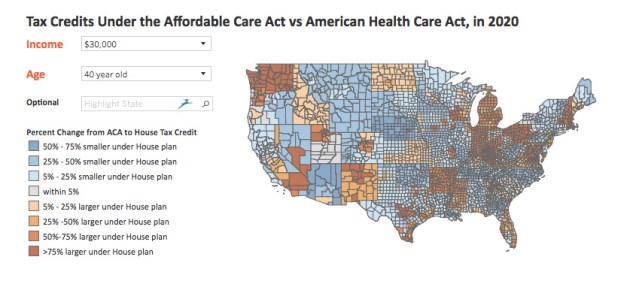

Many of the current plans for repealing the Affordable Care Act contain similar provisions. From a draft proposal circulated in mid February:

Speaker Paul Ryan is a big supporter of interstate insurance sales. A policy paper he released last summer lists it as a key recommendation.

But we question whether Ryan really understands the conflicting policy implications of such a recommendation, because the same paper also contains the following:

States have been in the business of regulating health insurance for decades. They should be empowered to make the right tradeoffs between consumer protections and individual choice, not regulators in Washington. The federal role should be minimal and set a few broadly shared goals, while state governments determine how best to implement those goals in their own markets.

Sorry Speaker Ryan (and President Trump), you can’t have it both ways. Allowing insurance sales across state lines will inevitably lead to federal regulation of the insurance industry.

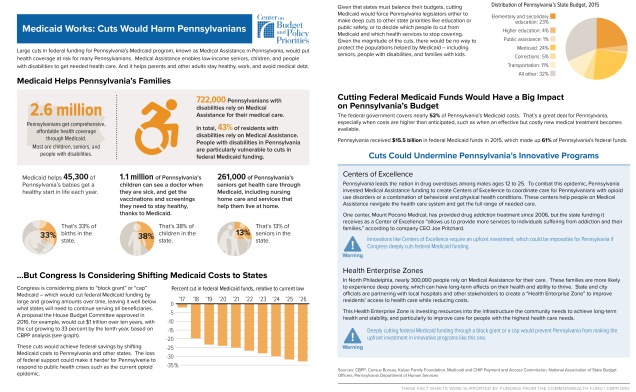

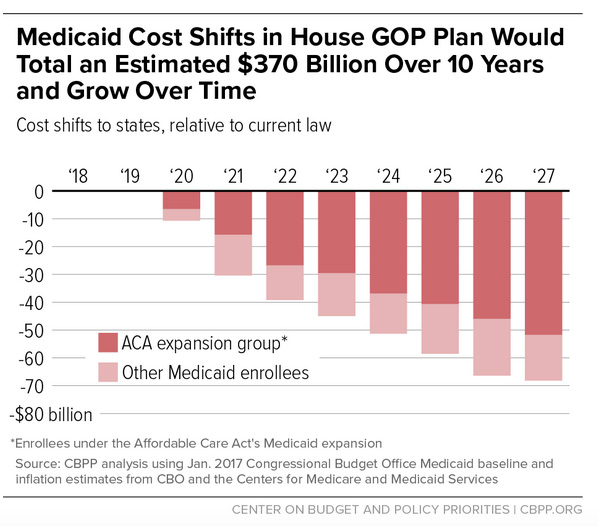

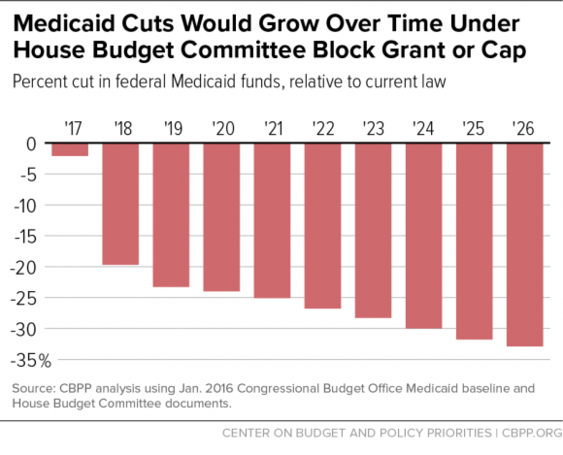

CBPP also created a series of fact sheets illustrating the effects of Medicaid cuts in nine different states. Here is the fact sheet for Pennsylvania:

CBPP also created a series of fact sheets illustrating the effects of Medicaid cuts in nine different states. Here is the fact sheet for Pennsylvania: