Medicaid

Why Insurance Companies May Provide Our Best Path to Universal Coverage

Don’t demonize insurance companies. I know it’s tempting. After all, they are trying to make money off of people’s health. But guess what? We live in a capitalist society and this is the system we currently have. Some type of single payer (and yes there are many versions, just look at the different countries in the EU) may be the ultimate progressive goal. But we can’t get there from here overnight. In fact, the only way we can get there is probably by bringing the insurance industry along.

The success of Medicaid Expansion under the Affordable Care Act is due in no small part to insurer participation in the Medicaid marketplace. Insurers specializing in the Medicaid market are profitable, and that’s a good thing.

Who do you think covers most of the people on Medicaid and many on Medicare? Who has the expertise? State Medicaid agencies contract with insurers to cover Medicaid beneficiaries. The insurance companies take on the risks, not the states. Similarly, many Medicare recipients chose to be covered by Medicare Advantage plans run by private insurers. Insurance companies are already deeply embedded in our so-called “entitlement” programs.

Right now everyone is worried about how to keep insurers in the individual market. The ACA originally provided several mechanism to help insurers deal with the uncertainty of the individual marketplace, including Risk Adjustments, Reinsurance, and Risk Corridors. You can find a good explanation of these three programs here.

The Risk Corridor program was supposed to last three years, ending in 2016. But it never really got a chance to work, because of a provision added to a must-pass 2015 budget bill by the Republican congress, requiring risk corridors to be revenue neutral. (At the time, Senator Marco Rubio characterized the risk corridors program as a bailout for insurance companies.) As a result, the federal government owes insurers billions of dollars, meant to offset losses on the exchanges. Several lawsuits are currently in progress. Is it any wonder some insurers have left the individual marketplace? Funding the risk corridor program and extending its life a few more years could help reverse this trend.

If the Feds aren’t up to the task, another solution for states with too few insurers offering policies on the individual marketplace is the “public option.” While this may seem like a more radical option, that’s not necessarily the case. I see two possible results:

-

Insurers would out-compete the public option, rendering it obsolete

-

Insurers would flee such markets, leaving only the public option.

But guess what? If that happened who do you think states would look to run their “public option” plans?

I keep seeing calls for “Medicare for All,” but why not make Medicaid available for everyone? After all, Medicaid in its current form (following ACA expansion) is the closest thing we have to what we all claim to want—a basic minimum level of healthcare for everyone. If you can afford more or have an employer who wants to offer you a better plan, then great (see the German system for example), but for everyone else, why not build on the part of the Affordable Care Act that already works best?

I can already anticipate some of the objections:

Giving people government handouts takes away their incentive to work.

Data on Medicaid expansion has shown this premise to be untrue. The majority of non-elderly non-disabled adults receiving Medicaid do work. They just earn too little to afford health insurance. And those who don’t work often have good reasons, like they are students or caregivers.

By expanding Medicaid to everyone, I’m not necessarily saying it should be “free” for everyone. But cost should not be a barrier to basic insurance coverage. People shouldn’t have to choose between healthcare and other necessities?

But people don’t appreciate free insurance or don’t use it wisely, aka they need “skin in the game.”

My short response to this is look at what happened when Indiana tried to charge Medicaid recipients small sums ($1 or $2) for their coverage. The bureaucratic costs outweighed the benefits.

The “skin in the game” hypothesis also assumes that people behave rationally when it comes to their health. But they don’t. They avoid going to the doctor because of high co-pays and deductibles, then end up in the emergency room when they get really sick. Or, they refuse to go to the emergency room when they should because of the high cost. They don’t comparison shop.

Medicaid reimbursements are too low/Most doctors don’t take Medicaid.

Whether this is true or not, should this be the main determinant? Everyone complains that healthcare costs keep going up. But then they complain when a program succeeds in cutting them. Plenty of doctors are willing to accept Medicaid. Doctors who treat low income patients consider Medicaid Expansion a game changer. They no longer have to scramble to get care for their patients. Hospitals also seem more than willing to accept Medicaid’s reimbursement rates. Yes, they might pass the cost on to others. But what do you think they did before, when they had much larger amounts of uncompensated care?

I’m no expert on Medicaid, and I am the first to admit “Medicaid for all who want it” is a long shot. But Medicaid is the part of the ACA that is currently working. The robust Medicaid market is helping prop up the individual marketplace. States that expanded their Medicaid programs have seen their individual marketplace perform better (with lower premiums). Support from Republican governors in Medicaid Expansion states certainly contributed to the widespread opposition to the AHCA.

As we look for ways to strengthen our healthcare system and move towards universal health insurance, we should build on the success of Medicaid expansion.

Infographics Part II: ACA Medicaid Expansion vs. AHCA Per Capita Caps

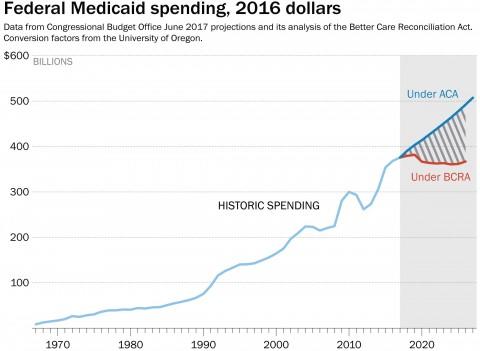

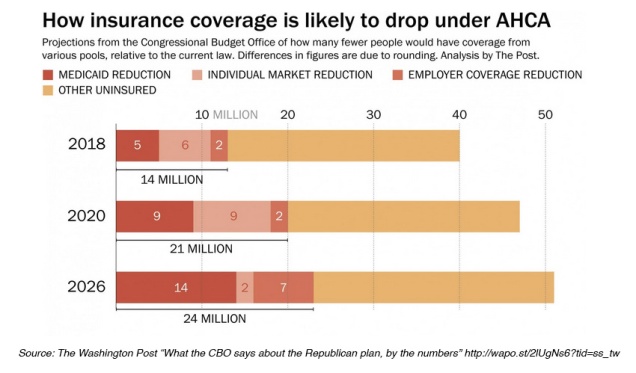

Medicaid beneficiaries stand to lose the most under the American Health Care Act (AHCA). According to the new Congressional Budget Office Report, Medicaid recipients would make up a disproportionately large share of 24 million people expected to lose health insurance coverage by 2026 if the GOP legislation becomes law.

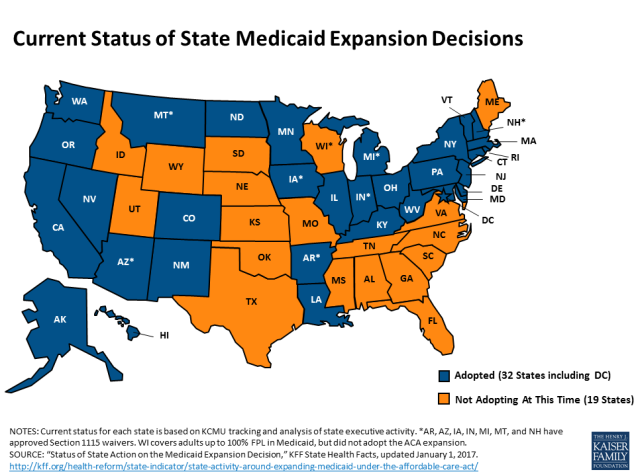

Under the Affordable Care Act (ACA) 32 states expanded Medicaid eligibility to low-income adults earning up to 138 percent of the poverty line (about $34,000 for a family of four). The AHCA, as currently written, continues expansion for three more years before cutting federal funding to state Medicare programs through a per capita cap, limiting coverage to those enrolled before 2020. Vox recently provided a good explanation of per capita caps as does the Kaiser Family Foundation.

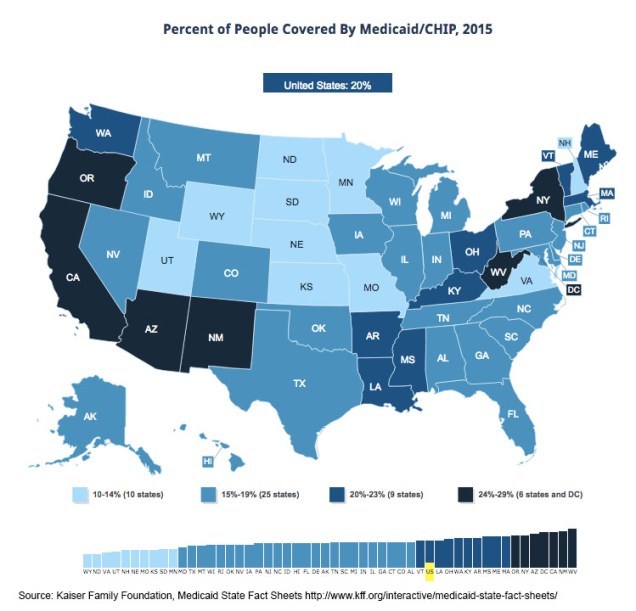

Many of the best Medicaid infographics predate the release of the AHCA, but they still remain relevant to the current discussion. The KFF website includes a large collection of data on Medicaid expansion, including maps (like the image above) and detailed Medicaid State Fact Sheets.

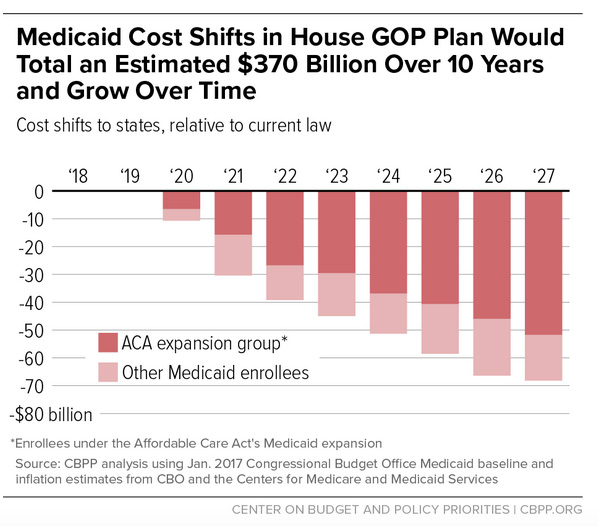

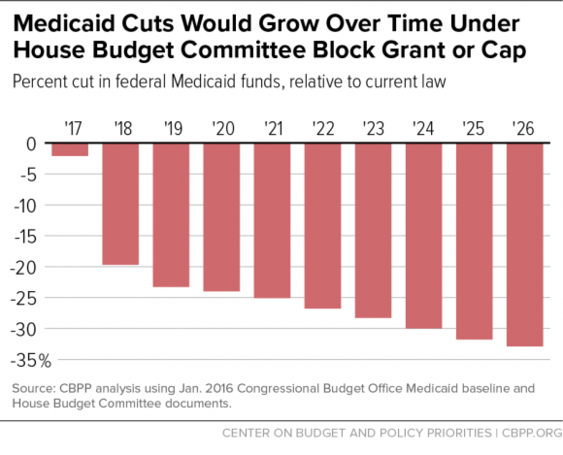

The Center on Budget and Policy Priorities (CBPP) produced the following charts estimating the costs to states of the per capita cap.

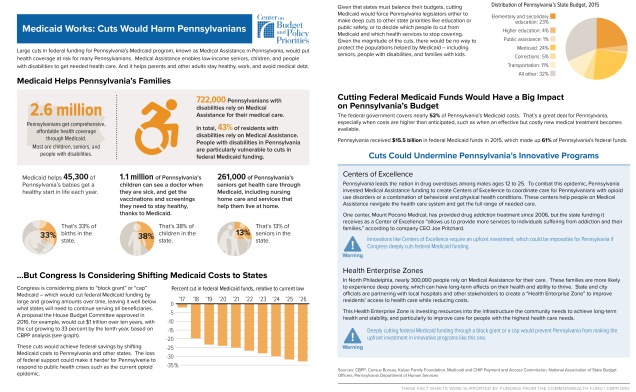

CBPP also created a series of fact sheets illustrating the effects of Medicaid cuts in nine different states. Here is the fact sheet for Pennsylvania:

CBPP also created a series of fact sheets illustrating the effects of Medicaid cuts in nine different states. Here is the fact sheet for Pennsylvania: