Part I: Tax Credits vs. Premium Subsidies

In the week since the Republicans unveiled their Obamacare replacement plan multiple news outlets have reported on what’s in the legislation, how it compares to the Affordable Care Act (ACA), who stands to benefit or lose, how much it will cost, etc.–many illustrated with helpful infographics.

Even if you follow the healthcare debate closely, the quantity of tables, graphs, and charts can quickly get overwhelming. After a while they all seem to look the same (actually, many are the same, or rely on the same data sources).

Want to know what’s in the American Health Care Act (AHCA) and how it might affect you and your community? We’ve compiled some of the best infographics from around the internet to help you make sense of it all.

Part I: Tax Credits vs. Premium Subsidies

One of the most significant changes in the GOP legislation is the replacement of premium subsidies (based on age, income, and geography) with age-and income-based tax credits, with no geographic variation. Several graphs from the Henry J. Kaiser Family Foundation (KFF) show how people of different ages and incomes fare under tax credits depending on where they live.(If you aren’t already familiar with the Henry J. Kaiser Family Foundation you should check out their website now.)

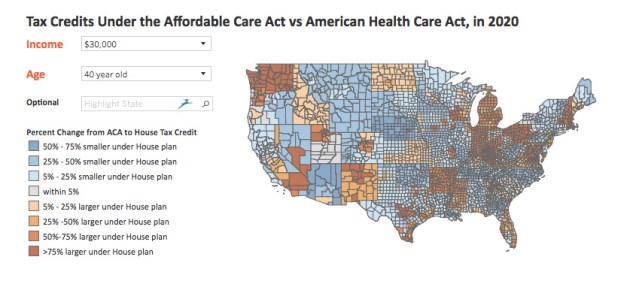

Their Interactive map provides county-and-state level comparisons of of ACA vs. AHCA tax credits based on age and income level.

Note: To try it out, click on the picture below to go to the KKF site. Once the new page opens, scroll down a bit to find the interactive map.

A related KFF report, How Affordable Care Act Repeal and Replace Plans Might Shift Health Insurance Tax Credits, includes the following charts, illustrating the effects of the GOP plan’s tax credits on individuals and families in different age and income groups in high and low cost states.

This slideshow requires JavaScript.

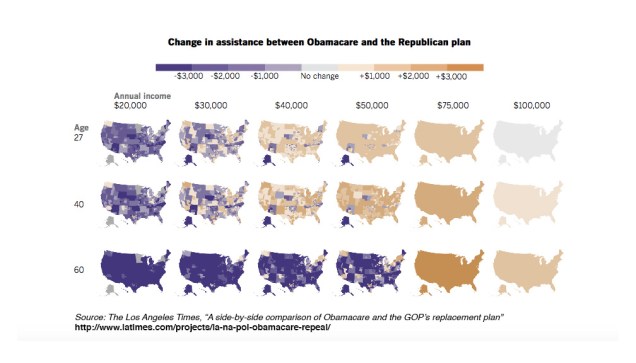

Many prominent news outlets cite KFF as a source for their illustrations. For example, last week, both The Los Angeles Times and The New York Times used similar graphics (in different colors) based on KFF data.

Another good set of illustrations of how the GOP plan might affect individuals at different income levels is provided in an analysis by The Century Foundation.

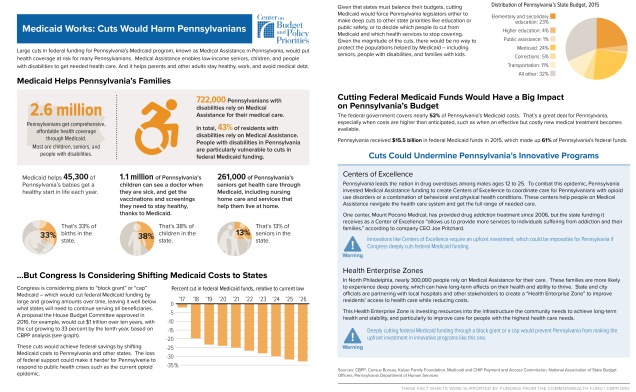

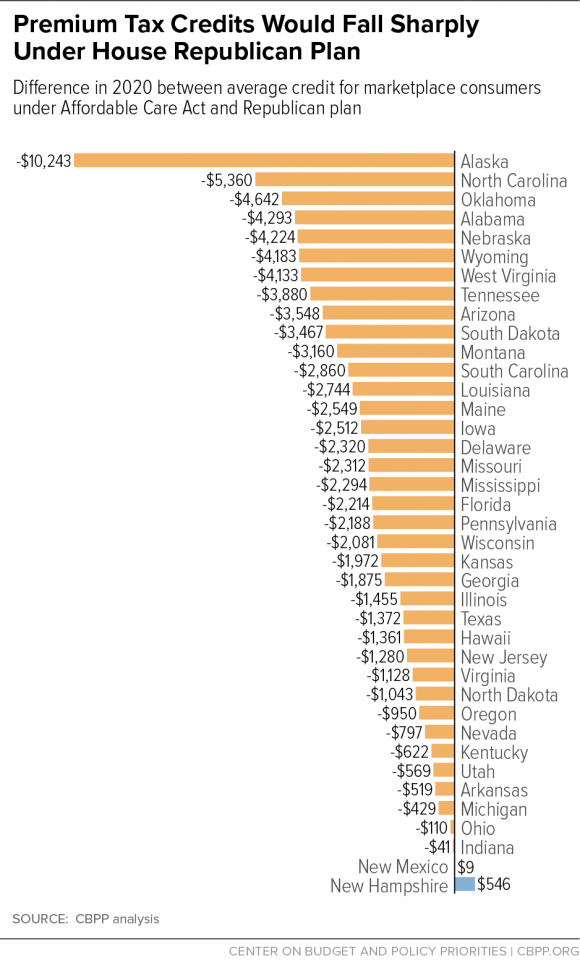

For a state-by-state comparison, the waterfall graph (below) from The Center on Budget and Policy Priorities (CBPP) shows the difference between the average ACA subsidy and the proposed AHCA tax credit.

Coming Soon:

Part III: Individual Mandate vs. Penalty for Break in Coverage

Part IV: Cost Comparisons